Here are a few key excerpts from the report.

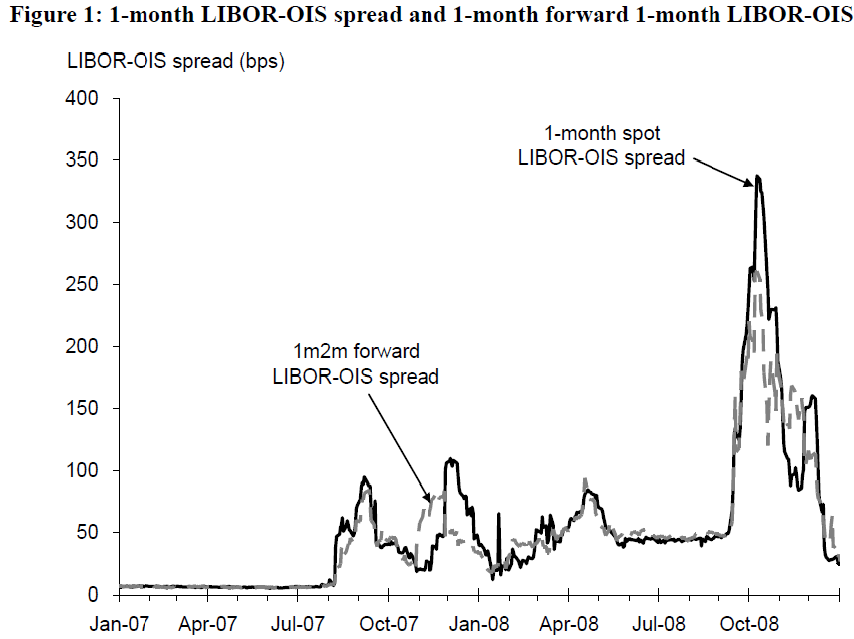

A better understanding of the forward-looking information content about funding liquidity risk in prices of interest-rate derivative instruments is necessary to improve the measurement of system-wide liquidity risk. Using the market prices, this paper derives the dynamics of the US-dollar LIBOR-overnight index swap (OIS) spread, which are considered as the funding liquidity risk premium and have been widely used by central banks to gauge funding liquidity conditions. We find that the dynamics contained significant probability of extreme price movements of the LIBOR-OIS spread during the crisis of 2008 reflecting deepened uncertainty about the funding liquidity risk.

The probability deviated from zero on 18 September 2008 to 12%, which provided an early warning signal of the systemic liquidity shock on 29 September 2008 when the interbank market was paralysed and the Federal Reserve authorised a US$330 billion expansion of swap lines with other central banks.

The information content about funding liquidity risk in prices of interest-rate derivative instruments could help the financial system be more prepared for liquidity shocks. The forward-looking probabilities of funding liquidity shocks derived in this paper could serve as a basis for the development of a set of potential early warning indicators, which could be used to indicate whether pressures on systemic liquidity are building up.Now that we know that this was a helpful indicator in 2008, let's take a look at what it is currently showing and if it is signaling anything important. The chart below is of the 1 month LIBOR-OIS spread for the last year. You can see that it did rise in May and June (reflecting European banking concerns), but the spread rose to a measly 16 bps. This is a far cry from the 300 +bps reached during the financial crisis in 2008; more importantly, the spread is already coming back down, indicating that credit concerns in Europe are easing. We can deduce at least for now that the probability of a banking crisis is currently low. But this is a useful indicator and serves as an early warning sign for potential trouble in capital markets.

Here is a link to bloomberg where you can find the indicator.

Black Swan Insights

http://www.voxeu.org/index.php?q=node/1188

ReplyDeleteFrancesco Giavazzi was asking this question back in June of '08.

He suggested predatory banks trying to take down other banks.

The banks have only themselves to blame for the problems their having.

DeleteI think the idea that banks were trying to take down each other is correct to a certain extent. JP Morgan was Lehman's clearing bank and according to documents filed in a lawsuit by some Lehman investors, JP Morgan issued a margin call for $38 billion. This was the event that forced Lehman into bankruptcy.

ReplyDelete